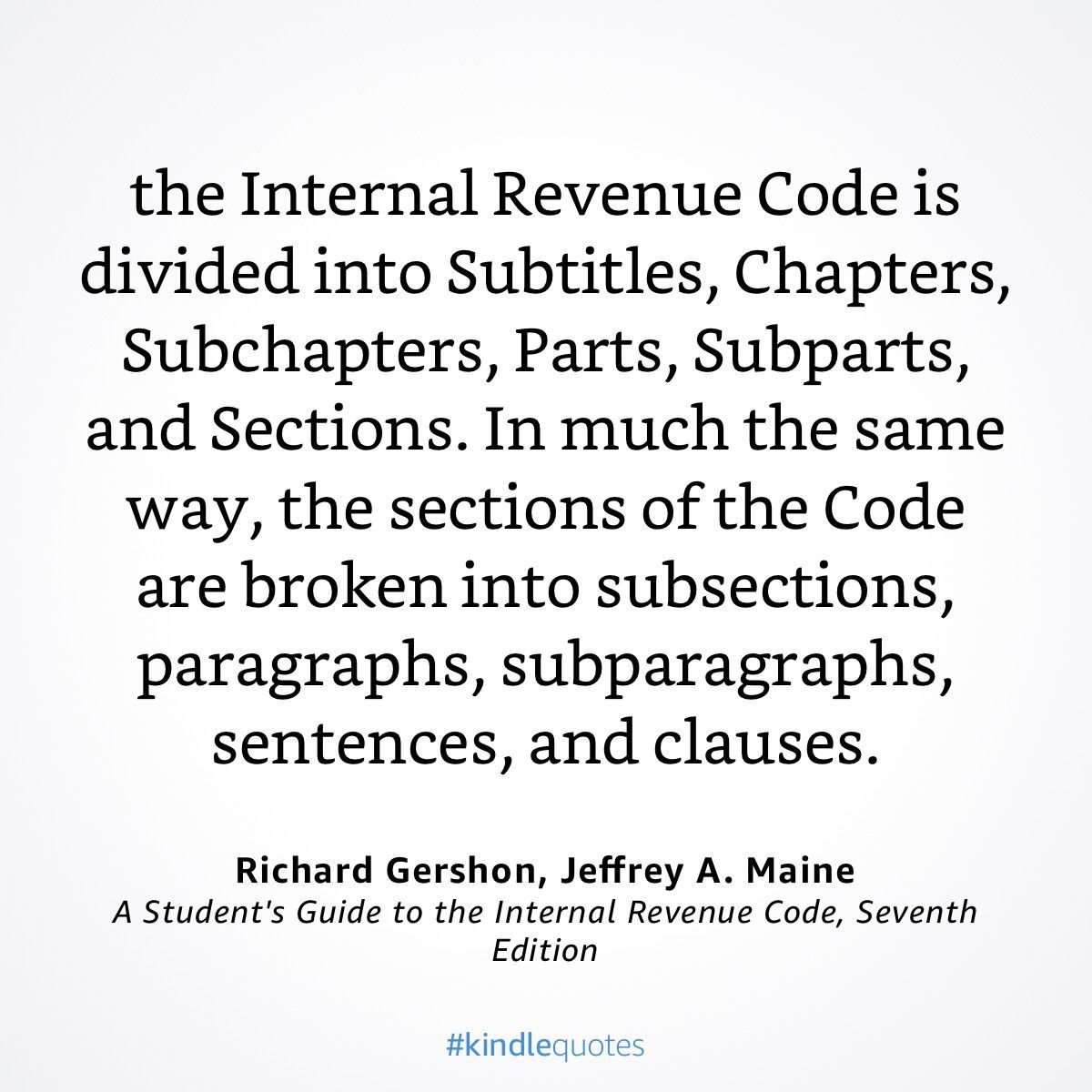

When talking about the Internal Revenue Code (IRC), knowing where you are and how to refer to it is important.

The quote above gives the structure of the Internal Revenue Code:

- Subtitle

- Chapter

- Subchapter

- Part

- Subpart

- Section

- Subsection

- Paragraph

- Sentence

- Clause

- Sentence

- Paragraph

- Subsection

- Section

- Subpart

- Part

- Subchapter

- Chapter

Knowing the structure of the IRC helps you when reading tax law.

For example, here is an excerpt from IRC § 1014 (with emphasis added):

- [SECTION] IRC § 1014 Basis of property acquired from decedent

- [SUBSECTION] (a) In general. Except as otherwise provided in this section, the basis of property in the hands of a person acquiring the property from a decedent or to whom the property passed from a decedent shall, if not sold, exchanged, or otherwise disposed of before the decedent’s death by such person, be—

- [PARAGRAPH] (1) the fair market value of the property at the date of the decedent’s death,

- . . .

- [SUBSECTION] (b) Property acquired from the decedent. For purposes of subsection (a), the following property shall be considered to have been acquired from or to have passed from the decedent:

- [PARAGRAPH] (1) Property acquired by bequest, devise, or inheritance, or by the decedent’s estate from the decedent;

- . . .

- [SUBSECTION] (e) Appreciated property acquired by decedent by gift within 1 year of death

- [PARAGRAPH] (1) In general. In the case of a decedent dying after December 31, 1981, if—

- [SENTENCE] (A) appreciated property was acquired by the decedent by gift during the 1-year period ending on the date of the decedent’s death, and

- [SENTNCE] (B) such property is acquired from the decedent by (or passes from the decedent to) the donor of such property (or the spouse of such donor),

- [FLUSH LANGUAGE] the basis of such property in the hands of such donor (or spouse) shall be the adjusted basis of such property in the hands of the decedent immediately before the death of the decedent.

- [PARAGRAPH] (2) Definitions. For purposes of paragraph (1)—

- [SENTNCE] (A) Appreciated property. The term “appreciated property” means any property if the fair market value of such property on the day it was transferred to the decedent by gift exceeds its adjusted basis.

- [SENTNCE] (B) Treatment of certain property sold by estate. In the case of any appreciated property described in subparagraph (A) of paragraph (1) sold by the estate of the decedent or by a trust of which the decedent was the grantor, rules similar to the rules of paragraph (1) shall apply to the extent the donor of such property (or the spouse of such donor) is entitled to the proceeds from such sale.

- [PARAGRAPH] (1) In general. In the case of a decedent dying after December 31, 1981, if—

- . . .

- [SUBSECTION] (a) In general. Except as otherwise provided in this section, the basis of property in the hands of a person acquiring the property from a decedent or to whom the property passed from a decedent shall, if not sold, exchanged, or otherwise disposed of before the decedent’s death by such person, be—

The words that are highlighted, above, show how the IRC refers to different places – such as the entire section, a paragraph, or a subparagraph.

Revenue Ruling 2023-2 is generally about one IRC section (§ 1014), but it is really about one clause in IRC § 1014(b)(1): "bequest, devise, or inheritance." Rev. Rul. 2023-2 is about whether property in certain irrevocable trusts that is not included in the grantor's gross estate will get stepped-up basis under IRC § 1014. While the grantor is alive, the grantor is treated as the owner of the trust's property for purpose of the income tax and the grantor pays the tax on any income. When the grantor dies, the trust property becomes the trust's for purposes of the income tax. The main question is whether this "transfer" for purposes of the income tax is a "bequest," "devise," or "inheritance" within the meaning of IRC § 1014(b)(1). The IRS concluded that the property doesn't meet the definitions of any of these terms, but I recently observed that the full definition of just one word, "bequest," from the dictionary that the IRS cites (Black's Law Dictionary) invites a different conclusion.

Hani Sarji

New York lawyer who cares about people, is fascinated by technology, and is writing his next book, Estate of Confusion: New York.

{kind=link}

Leave a Comment