New York Assembly Bill A08549-A proposes a major change in how joint bank accounts are treated under New York law.

It creates a new category—spousal joint accounts (proposed BL § 675-a)—which include automatic survivorship rights. But here’s the catch: only married couples can open these new accounts.

For everyone else—siblings, friends, unmarried partners—joint ownership with survivorship is no longer the default. Instead, these relationships are limited to non-spousal accounts (proposed BL § 675-b), where the depositor remains the sole owner during life and no survivorship rights attach unless expressly added.

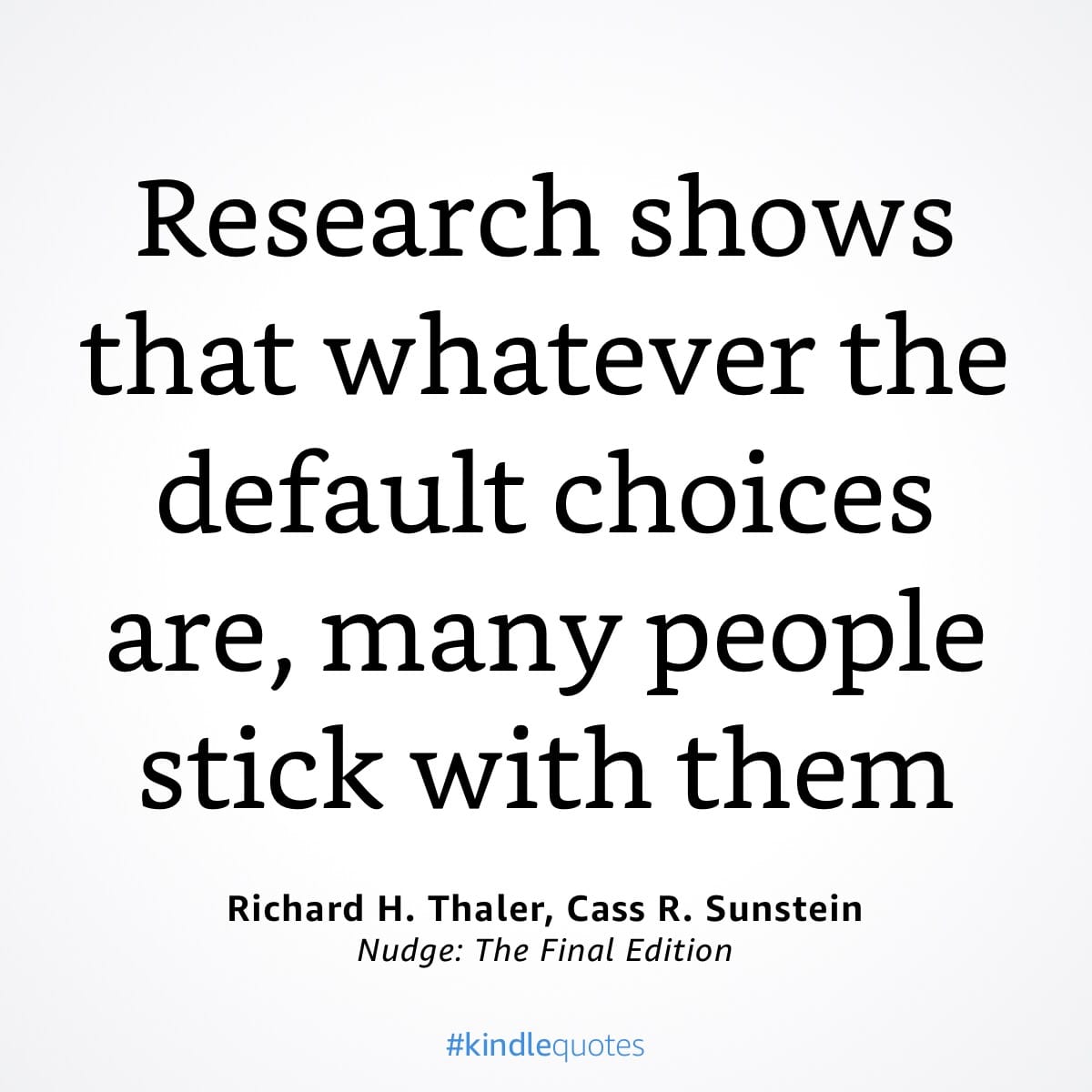

This shift is likely to increase probate filings. That’s not a speculative worry—it’s a predictable result supported by behavioral economics.

Behavioral economists Richard H. Thaler (Nobel Prize, 2017)[1] and Cass R. Sunstein (Holberg Prize, 2018)[2] have shown that people overwhelmingly stick with default settings.[3]

This insight has been confirmed in many contexts—from organ donation[4] to retirement savings. When the law shifts the default, human behavior reliably follows.

If those promoting the bill are aware of this and choose not to address it, then it’s fair to infer that this result is either intended or acceptable to them.

{kind=link}

Leave a Comment